This former penny share has quadrupled. Could it go higher?

Picture supply: Getty Photos

A variety of penny shares are in obscure corporations most individuals have by no means heard of. However not all. Take ME Group (LSE: MEGP) for example. 4 years in the past, the corporate was buying and selling firmly in penny share territory. Since then, it has greater than quadrupled, because of stable earnings and money flows.

When you might by no means have heard of the corporate, there’s a truthful likelihood you’ve got seen (and even used) one among its hundreds of picture machines in supermarkets, purchasing centres, and elsewhere, or one among its RevolutIon laundry machines.

Engaging enterprise mannequin

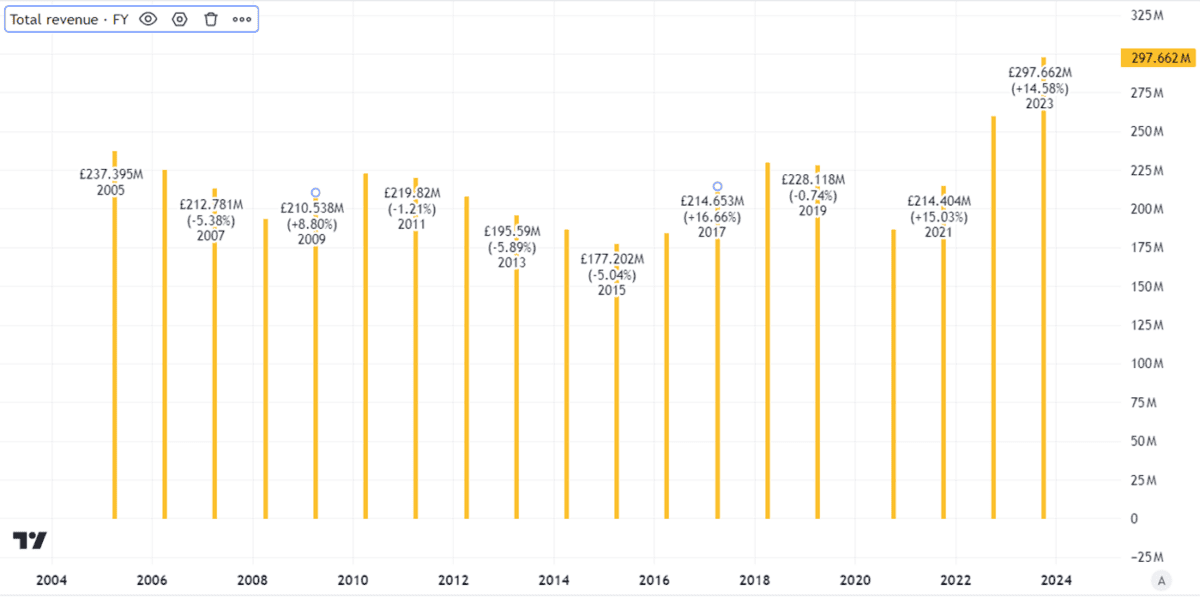

This can be a profitable enterprise. The corporate operates in areas which have excessive demand. Even throughout the depths of the pandemic, when ME Group was buying and selling as a penny share, revenues fell however didn’t collapse.

Created utilizing TradingView

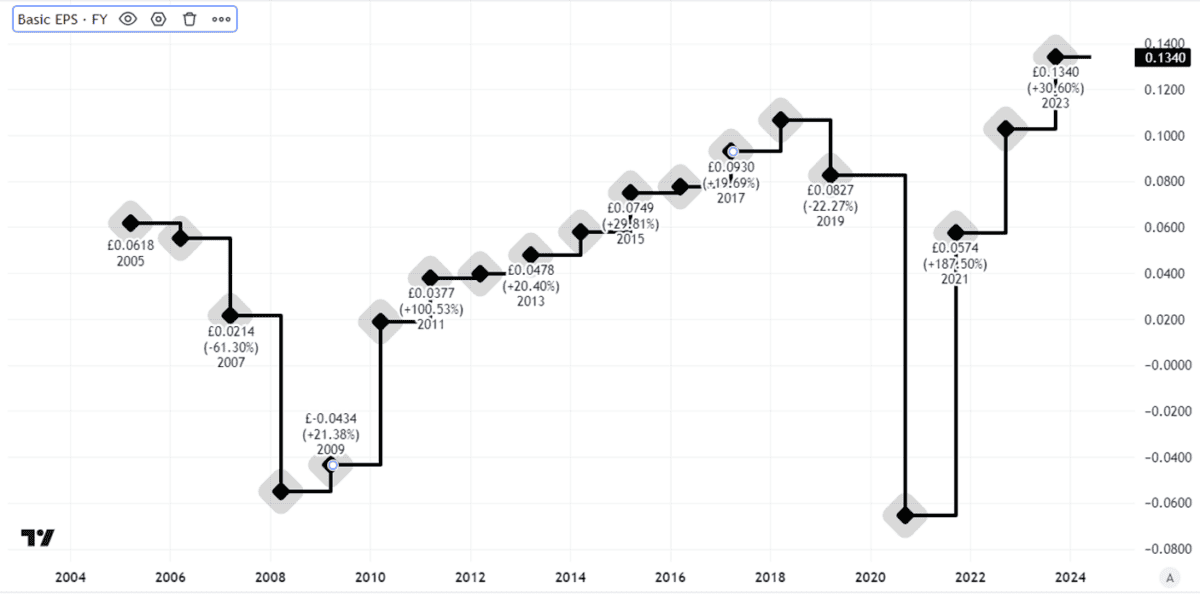

On the subject of profitability, earnings have moved round.

Even earlier than the pandemic earnings per share had declined – and so they took a pummelling over the following a number of years, serving to clarify why ME was buying and selling as a penny share.

Created utilizing TradingView

However because the chart above reveals, they’re now stronger than they’ve ever been. I believe that speaks to the attraction of ME’s enterprise mannequin: its automated machine community signifies that its labour prices will be stored low, whereas the providers it gives are inclined to have sturdy demand. If folks have to do their laundry, they should do their laundry.

Valuation may supply long-term worth

However enterprise doesn’t essentially make funding. Valuation issues too.

I believe ME Group stacks up pretty properly on that entrance. Trying on the present price-to-earnings ratio of 13, I believe it gives the potential for long-term appreciation if earnings per share proceed to extend in future.

On prime of that, the dividend yield of 4.3% appears to be like engaging to me.

I believe the corporate’s distinctive property of machines and lengthy expertise of merchandising machines helps set it other than opponents. However there are dangers. As we noticed throughout the pandemic, any drop within the variety of folks visiting purchasing centres can result in a pointy drop in demand.

Purchase or wait?

Having been a penny share inside the final 4 years, although, may ME Group head again there any time quickly?

Something is feasible within the markets, after all, however for now not less than I believe the agency’s sturdy enterprise efficiency is more likely to maintain the share worth buoyant. Its lack of competitors in lots of areas provides it pricing energy, which I believe may imply we see even larger earnings in future.

So, despite the fact that it not gives the screaming worth it did as a penny share, if I had spare money to speculate right now I’d be glad so as to add ME Group to my portfolio.