Builders finally making a dent in Colorado’s housing shortfall. It’s not helping buyers or renters.

Builders are lastly making a dent within the state’s housing shortfall, particularly for flats. However house costs and mortgage charges proceed to outpace revenue positive aspects, and affordability is worsening reasonably than enhancing.

“The story with rates of interest is that they’re solely exacerbating the issue,” mentioned Steven Byers, chief economist with the Frequent Sense Institute in Denver. “The very fact is that wages aren’t maintaining with these large jumps in house costs.”

For the primary time since July 2022, house costs in all main U.S. metros, together with Denver, rose year-over-year, stories brokerage agency Redfin. The S&P CoreLogic Case-Shiller Index for Denver has house costs up 2.7% the previous yr by way of February.

After 5 weeks of will increase, the typical rate of interest charged on a 30-year mortgage reached 7.22%, the best stage since Thanksgiving, based on Freddie Mac.

Buying a house was arduous earlier than, and it’s only getting tougher. In 2011, a purchaser in Colorado may count on to work 44 hours a month on common to cowl the mortgage fee. That bar moved as much as 96 hours final yr, a 118% improve, based on CSI’s Colorado Housing Competitiveness Index, which Byers co-authored.

Issues are solely barely higher for renters. They needed to work 45 hours on common to cowl the month-to-month hire in 2011. Now they need to work 87 hours. Colorado tenants dedicate extra hours of labor a month to fulfill the hire than do residents of another state, based on the CSI report.

After the Nice Recession, metro Denver turned a scorching spot for younger professionals and tech staff seeking to relocate. Demand for housing outstripped provide, inflicting house costs and rents to rise. Web home migration has fallen the previous two years, as extra individuals choose up and depart and fewer transfer in, Byers mentioned. Increased housing prices have made the state much less enticing.

That’s each good and unhealthy. Slower inhabitants progress ought to cut back stress on the housing market and provides builders time to catch up, stabilizing house costs and rents over time. However it additionally leaves employers and the bigger financial system, lengthy depending on importing the expertise it wants, susceptible. If the financial system stalls, these combating larger dwelling prices may pay the value.

Of the 50 largest U.S. metro areas, solely six have median house costs that align with median incomes, based on a research from Intelligent Actual Property. Denver had the eighth largest hole between within the quantity of revenue wanted to achieve a median-priced house.

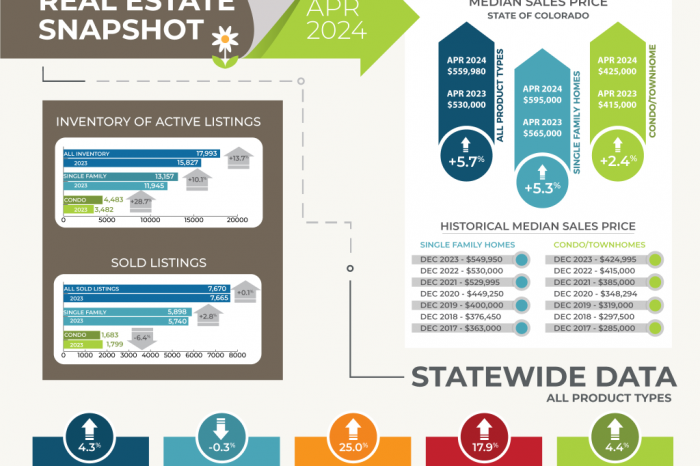

Zillow locations the everyday house worth in metro Denver at simply shy of $561,000 in December. Assuming a 20% downpayment and at present mortgage charges, an annual revenue of $167,562 can be required to purchase that house, based on the Intelligent Actual Property research.

However right here’s the place it will get painful. The median revenue for metro Denver households is $98,975 a yr, leading to a shortfall of $68,587. Denver residents earn above-average incomes, however the larger pay isn’t sufficient to cowl manner above-average housing prices.

Wages are usually decrease in different elements of the state, and the affordability “hole” statewide is slightly bigger at $69,587. Colorado’s median house value is $531,900, not too far behind the metro Denver median value. With 20% down, that requires an revenue of $158,889, based on Intelligent Actual Property. The median family revenue statewide is $89,302.

Absent exterior assist, first-time consumers are sometimes hard-pressed to place 20% down. That may require $112,200 on the everyday house in Denver. What may somebody placing 10% down and making the median revenue in Denver afford after the current leap in mortgage charges? Intelligent Actual Property places that quantity nearer to $270,000 to $280,000.

Good luck discovering that. Out of 6,458 single-family house closings in metro Denver within the first three months of the yr, solely 50 concerned a house priced under $300,000, based on the Denver Metro Affiliation of Realtors.

Patrons of condos and townhomes face higher odds, with 452 out of two,343 gross sales this yr under $300,000. However even there, solely 20% of listings are inexpensive to households incomes a median revenue. Solely 5.7% of gross sales, houses or condos, had been attainable.

The hurdle is even larger for brand new house consumers. The median new house value in Colorado is about $650,000, based on a research from the Nationwide Affiliation of Homebuilders. Just one in 5 households within the state can afford one thing at that value level. Two million households within the state can’t afford to buy a brand new house on the center value level.

Renting cheaper now, however expensive long-term

Most renters have restricted choices in terms of shopping for in metro Denver. However of their favor, renting affords a considerable low cost over shopping for proper now, based on a separate evaluation from Bankrate, the non-public finance web site.

The standard month-to-month fee for the median-priced house is round $3,627 in metro Denver, together with the mortgage fee, property taxes and insurance coverage. Against this, the everyday hire is $2,027 when a hire index from Zillow that mixes residence, rental and residential rents.

Renting was cheaper than shopping for in all 50 metros studied, however Denver had the ninth largest hole at $1,600. That 79% premium was a lot bigger than the 36.6% premium to personal nationally.

“I wouldn’t say hire is inexpensive, however between shopping for and renting, renting is the lesser of the 2 evils,” mentioned Alex Gailey, lead knowledge reporter at Bankrate and the creator of the evaluation.

In a super world, renters would sock away that extra cash as emergency financial savings. After that, financial savings can be invested within the inventory market, which has supplied the next return than proudly owning a house over time. If an employer matches a retirement plan contribution, that may translate into an computerized 50% return off the bat.

However most renters in all probability gained’t observe that technique, leaving them susceptible long-term, Gailey acknowledges. If an space isn’t shedding inhabitants, houses ought to rise in worth even after accounting for repairs and upkeep.

That fairness could be poured into shopping for an even bigger house down the street, or it might assist fund bills in retirement or be handed onto kids and heirs, constructing inter-generational wealth. Additionally, mortgage funds could be locked in, whereas a hire fee can’t.

“You might be constructing fairness for your self reasonably than for another person,” mentioned Jen Ankrum, director of gross sales for KB House in Colorado, when requested concerning the message the corporate shares with renters seeking to purchase.

First-time consumers account for about half of the gross sales at KB House, which strives to supply a high-quality, energy-efficient house priced under the competitors. Even with the heavy deal with first-timers, a couple of third of consumers make below $100,000, a 3rd make $100,000 to $150,000 and a 3rd make greater than that quantity.

Usually, the housing market tries to seek out an equilibrium, offsetting rising curiosity prices with slower value positive aspects and even value declines. However demographics have prevented that from occurring. Millennials, born between 1981 and 1996, are actually the nation’s largest technology at 72 million. They’re not on time in comparison with prior generations in terms of shopping for houses and pushing arduous to accumulate them even when the circumstances aren’t favorable.

Markets the place extra millennials relocated to have housing markets below probably the most stress. A little bit greater than six in 10 homebuyers in metro Denver are millennials — solely San Francisco and San Jose in California and Boston have the next share of millennial consumers, based on a research from mortgage portal LendingTree.

None of these markets can be thought-about inexpensive. In Denver, millennial consumers on common made a downpayment of $70,710 and borrowed $456,805 to buy a house, LendingTree stories.

“A giant motive why millennials focus in costly housing markets is as a result of these areas typically have sturdy and comparatively high-paying job markets,” mentioned Jacob Channel, a senior economist at LendingTree and creator of the report.

Massive tech corporations are decreasing their headcounts and a recession, when it comes, may speed up layoffs. What occurs if these high-paying jobs go away however the excessive mortgage funds don’t? However Channel doesn’t see a systemic threat to the housing market.

“Whereas there are doubtlessly some millennials who’re at present stretched too skinny and should deal with the prospect of downsizing or, within the worst case, foreclosures, the variety of individuals struggling isn’t massive sufficient for there to be a severe threat to the broader housing market,” Channel mentioned.

Get extra actual property and enterprise information by signing up for our weekly publication, On the Block.

Trending Now

The Origins and History of Lizard People

You may also like