With an 8% dividend yield, I think this undervalued FTSE stock is a no-brainer buy

Picture supply: Getty Photos

I’m as soon as once more evaluating potential FTSE shares so as to add to my dividend portfolio. Shares that pay a dependable dividend assist to make sure my portfolio offers constant returns. Nonetheless, I want to have a look at extra than simply the dividend yield to know which shares make the very best additions.

At the moment I’m contemplating one of many UK’s most well-known excessive avenue banks, HSBC (LSE:HSBA). Barclays has already confirmed worthwhile for me this yr and I’m hoping HSBC can do the identical by way of dividends.

Its 8% dividend yield is greater than the 6.8% trade common. Plus, a payout ratio of 53% means the dividend is well-covered by earnings so funds are more likely to be dependable and constant. This can be a key metric to examine when contemplating dividend shares.

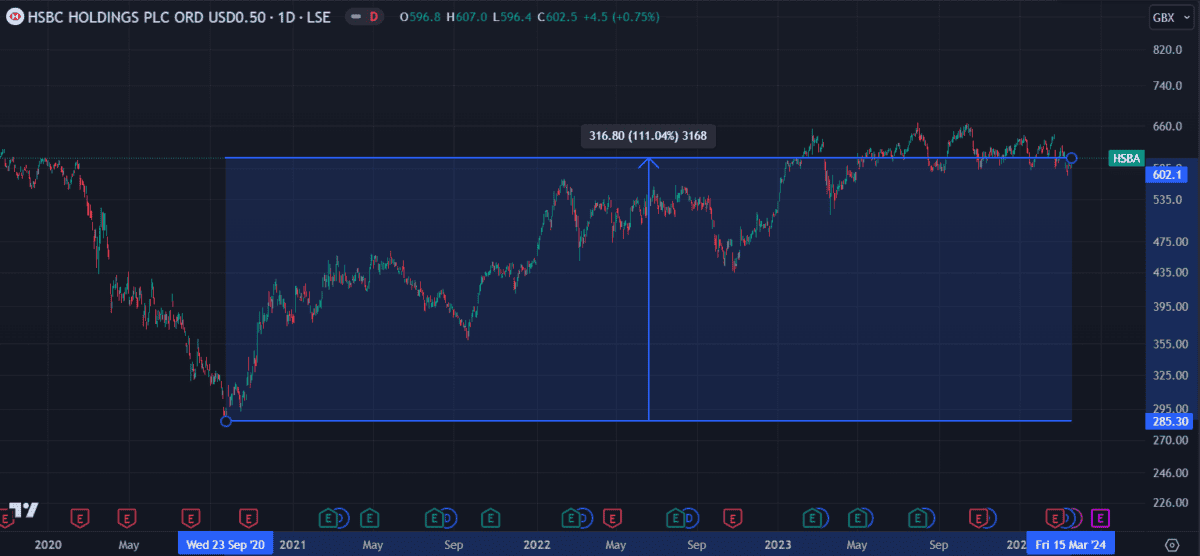

Subdued progress

The HSBC share worth has loved solely gentle progress over the previous 4 years from a low of two.8p in late 2020. Now at 6p a share, it’s up 111% since then — however barely down from a excessive of 6.6p in October 2023.

Nonetheless, the newest earnings report was not fully optimistic. Whereas income was in keeping with expectations, earnings-per-share (EPS) fell beneath analyst expectations by 13%. The subdued share worth means forecasts estimate HSBC to be undervalued by 57%. That is supported by a low price-to-earnings (P/E) ratio of 6.6, barely beneath the trade common of seven.4.

Robust dividend forecast

Based mostly on a mean of forecasts from a variety of analysts, the consensus is that HSBC’s dividend funds will enhance within the coming years. Along with an estimated enhance to eight.4% by 2027, HSBC has additionally promised a particular dividend of 21p per share paid out when it sells its Canadian division.

An upcoming dividend of 31p per share might be paid out on 25 April for any shareholders who purchased earlier than 7 March 2024. Sadly, I missed that ex-dividend date however I plan to get in earlier than the following one.

Dangers

The most important threat the banking trade faces is an financial slowdown or recession, a state of affairs that sometimes leads to mortgage defaults. It’s no secret that previous recessions have led to financial institution closures.

To guage this threat we have to have a look at the financial institution’s stability sheet.

As of 30 December 2023, HSBC was estimated to have round £500bn in complete debt and solely £150bn in fairness. This could end in a debt-to-equity (D/E) ratio of 332% – a quantity ideally saved beneath 100%. However a extra regarding determine is the financial institution’s allowance for dangerous loans, which at 57%, is taken into account inadequate. Ideally, this quantity must be above 100%.

This places it liable to losses if a worsening financial system results in a rise in mortgage defaults.

Web optimistic

Regardless of the dangers, I feel HSBC has the potential for a internet optimistic final result to my portfolio. Latest efficiency suggests the share worth may proceed to get pleasure from gradual however steady progress from right here.

Even within the occasion of worth depreciation, the excessive dividend yield would assist to offset losses. Because of this, I really feel assured so as to add HSBC to my checklist of dividend shares for my subsequent shopping for spherical.